Emphasizing the Fed's dilemma.

On Dec. 15 2021

the Federal Reserve Chair Jerome Powell said that inflation is now enemy No. 1

to keeping the economic expansion on track and returning the labor market to

something approaching ebullient pre-pandemic levels. Additionally, it would end

its pandemic-era bond purchases in March and pave the way for three

quarter-percentage-point interest rate hikes by the end of 2022 as the economy

nears full employment and the U.S. central bank copes with a surge of

inflation.

Well; easy to say

as usually but the dilemma comes with numbers; and What did I told

you?

First of all, I

want you to realize that Jerome Powell at the next policy settings as of the

Federal Open Market Committee hold on Dec 14-15, he Jerome Powell publicly will

announce with whatever statement he will made, that Albert Einstein was right, and that the law

of mathematics forces the FOMC committee to reduce asset purchase. But … not

because of COVID-19 pandemic … but because, they do not have liquidity assets to

keep that pace of securities purchase as of 120 billion U.S.

dollars.

First of all, I

want you to realize that Jerome Powell at the next policy settings as of the

Federal Open Market Committee hold on Dec 14-15, he Jerome Powell publicly will

announce with whatever statement he will made, that Albert Einstein was right, and that the law

of mathematics forces the FOMC committee to reduce asset purchase. But … not

because of COVID-19 pandemic … but because, they do not have liquidity assets to

keep that pace of securities purchase as of 120 billion U.S.

dollars.

At this time, we

have to emphasize the Fed's dilemma … If it raises interest rates, that raises

the U.S. debt-service costs. So, before Federal Reserve Chair Jerome Powell

approaches this dilemma for a congressional form of loan or considers what rate

of interest on that loan has to be set-offer for a bond issue as new form of

security purchase that has been or rather is in wrapping up the taper of our

asset purchases, the Fed’s needs to compute

the debt service coverage ratio. This ratio helps to determine the borrower’s

ability to make debt service payments because it compares the net operating

income with the amount of principal and interest the firm must pay. … 100% debt

to GDP means that 4-6% interest rates translate to 4-6% of GDP extra deficit,

may be as high as $1 trillion for every year interest rates. If the government

does not tighten by that amount, either immediately or credibly in the near

future, then the higher interest rates must ultimately raise, rather than lower,

inflation. At the end it’s appeared that it might not be able to roll over its

debt and default.

At this time, we

have to emphasize the Fed's dilemma … If it raises interest rates, that raises

the U.S. debt-service costs. So, before Federal Reserve Chair Jerome Powell

approaches this dilemma for a congressional form of loan or considers what rate

of interest on that loan has to be set-offer for a bond issue as new form of

security purchase that has been or rather is in wrapping up the taper of our

asset purchases, the Fed’s needs to compute

the debt service coverage ratio. This ratio helps to determine the borrower’s

ability to make debt service payments because it compares the net operating

income with the amount of principal and interest the firm must pay. … 100% debt

to GDP means that 4-6% interest rates translate to 4-6% of GDP extra deficit,

may be as high as $1 trillion for every year interest rates. If the government

does not tighten by that amount, either immediately or credibly in the near

future, then the higher interest rates must ultimately raise, rather than lower,

inflation. At the end it’s appeared that it might not be able to roll over its

debt and default.

Central banks

first stop bond buying and then raise interest rates. By keeping down the

risk/default premium in that rate, but there is no question that the bond buying

keeps down interest rate. If the Fed’s stops buying or removes the commitment to

purchases, debt service costs will rise again precipitating the slow decay.

Whether U.S. bond buying programs actually lower treasury yields is or rather be

debatable.

Central banks

first stop bond buying and then raise interest rates. By keeping down the

risk/default premium in that rate, but there is no question that the bond buying

keeps down interest rate. If the Fed’s stops buying or removes the commitment to

purchases, debt service costs will rise again precipitating the slow decay.

Whether U.S. bond buying programs actually lower treasury yields is or rather be

debatable.

The FED’s also

knows, that if it tightens monetary policy, i.e. stop asset purchases and raise

rates, debt-burdened will face severe challenges. The FED’s also knows, that

very expansionary monetary policy, combined with already high inflation and

strong economic growth, creates a serious risk that inflation and inflation

expectations run wild.

Let me quote at

this point Mohamed A. El-Erian - In a move labeled by some as a hawkish pivot

and by others as a great reset, the Federal Reserve’s policy committee just went

in one meeting from its often-repeated characterization of inflation as

“transitory” to portraying it as the “No. 1 enemy” facing the economic recovery.

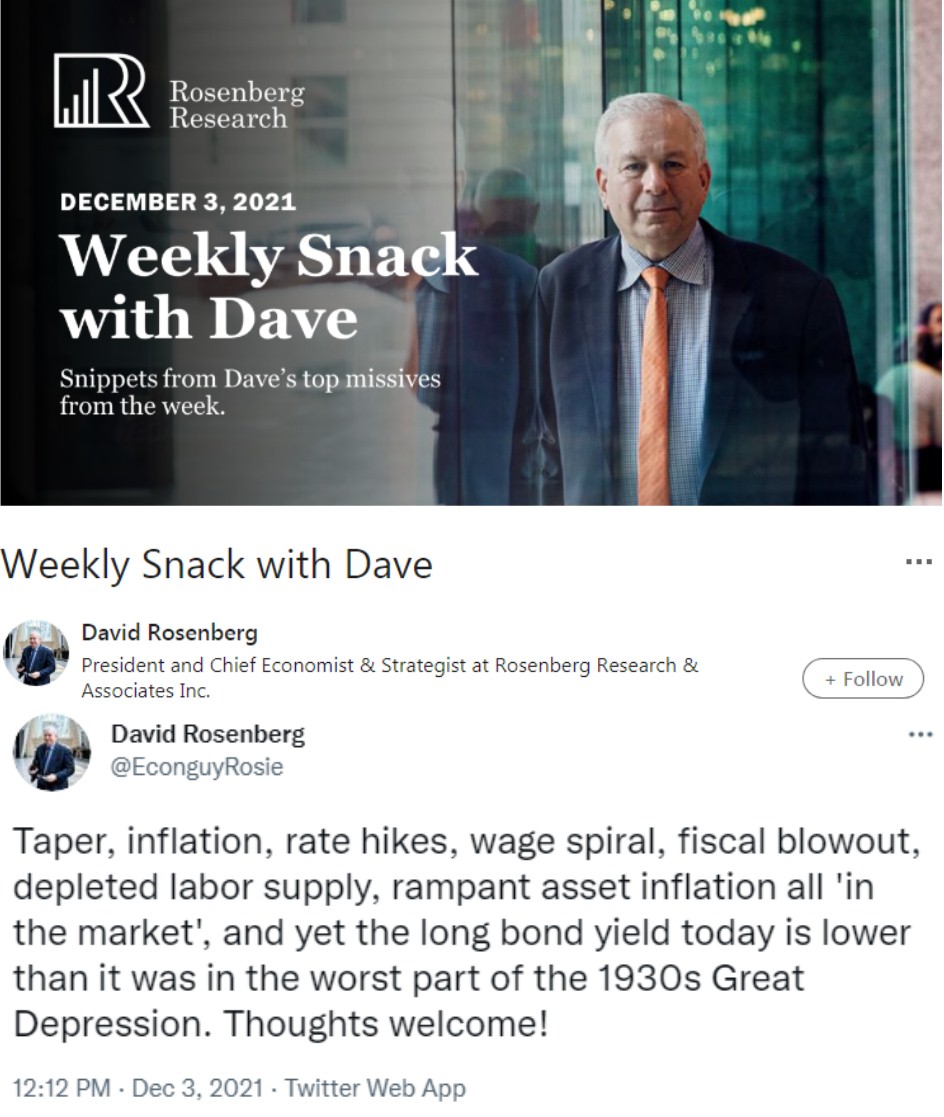

What has been also pointed by David Rosenberg Chief Economist & Strategist

of Rosenberg Research & Associates Inc. as; … The word “transitory” was

dropped, as advertised, and the taper of the balance sheet is doubling in size

to $30 billion per month from $15 billion. The “dot plots” were more hawkish but

caught up with the market — the median is now at three hikes for next year (up

from one) and another three for 2023.

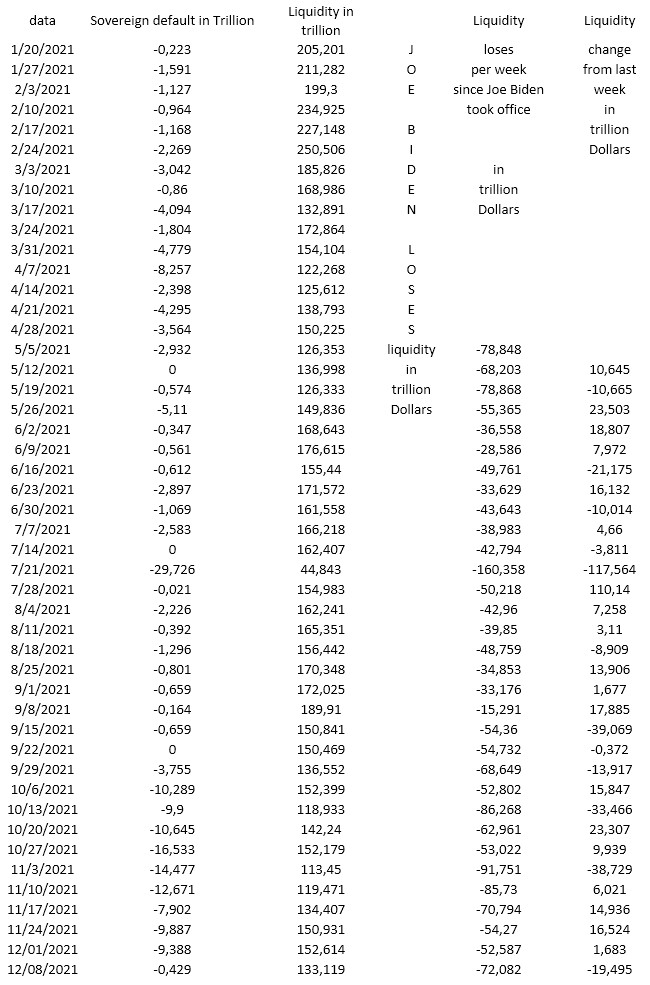

In conclusion let’s take a

look as how the United States wallet looks like in genuine reality as Primary

Dealers assets known as liquidity.

In conclusion let’s take a

look as how the United States wallet looks like in genuine reality as Primary

Dealers assets known as liquidity.

The cycle of the

conversion as transformation from liquidity to sovereign GOV default in Trillion

and vice versa, remaining a reverse spiral as its getting smaller and

smaller.

Before on July

2021 the US sovereign default reach the highest point in sovereign GOV default

as - $29,726 in trillion. At this time has been split to 10

smaller sovereign GOV default which bring us total to -$101,692 in trillion. It

looks like Jerome Powell is better magician then the Fed’s

chairman.

By Peter von Roggenhausen Dec. 18 2021.