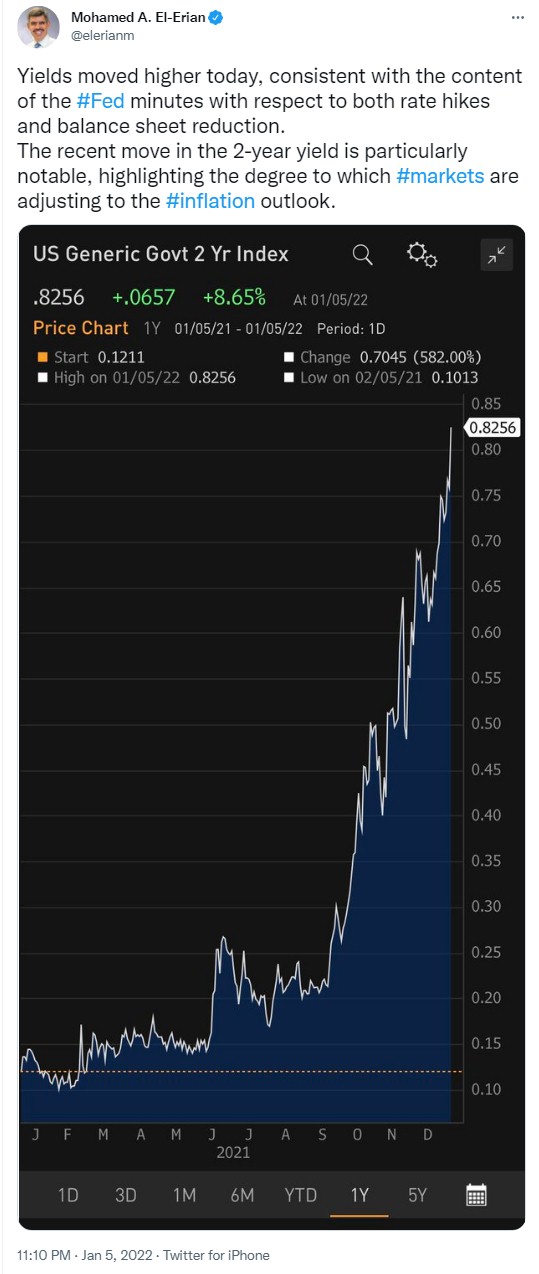

Will the Federal Reserve balance sheet … as of its initiate runoff ... would be data dependent?

A joint meeting of the

Federal Open Market Committee and the Board of Governors of the Federal Reserve

System was held by videoconference on Tuesday, December 14, 2021, at 9:00 a.m.

and continued on Wednesday, December 15, 2021, at 9:00 a.m. But the minutes of

this meeting were released yesterday on January the 5 2022. In response, the

Propaganda Machine as Reuters for that instance followed by Bloomberg, CNBC or

Fox News etcetera, imprinted to general bread consumers reality perception that

the strengthening economy and higher inflation could lead to earlier and faster

interest-rate increases than previously expected, with some policy makers also

favoring starting to shrink the balance sheet soon after.

A joint meeting of the

Federal Open Market Committee and the Board of Governors of the Federal Reserve

System was held by videoconference on Tuesday, December 14, 2021, at 9:00 a.m.

and continued on Wednesday, December 15, 2021, at 9:00 a.m. But the minutes of

this meeting were released yesterday on January the 5 2022. In response, the

Propaganda Machine as Reuters for that instance followed by Bloomberg, CNBC or

Fox News etcetera, imprinted to general bread consumers reality perception that

the strengthening economy and higher inflation could lead to earlier and faster

interest-rate increases than previously expected, with some policy makers also

favoring starting to shrink the balance sheet soon after.

But what they as

the Propaganda Machine shall tell for you … goes like

this;

The Federal Open

Market Committee also observed that the Federal Reserve’s balance sheet was much

larger, both in dollar terms and relative to nominal gross domestic product

(GDP), then it was at the end of the third large-scale asset purchase program in

late 2014. Participants noted that the current weighted average maturity of the

Federal Reserve’s Treasury holdings was

shorter than at the beginning of the previous normalization episode as of

2014. Some observed that, as a result, depending on the size of any caps put on

the pace of runoff, the balance sheet could potentially shrink faster than last

time if the Committee followed its previous approach in phasing out the

reinvestment of maturing Treasury securities and principal payments on agency

MBS. … they noted that current conditions included a stronger economic outlook,

higher inflation, and a larger balance sheet and thus could warrant a

potentially faster pace of policy rate normalization. They emphasized that the

decision to initiate runoff would be data dependent.

The Federal Open

Market Committee also observed that the Federal Reserve’s balance sheet was much

larger, both in dollar terms and relative to nominal gross domestic product

(GDP), then it was at the end of the third large-scale asset purchase program in

late 2014. Participants noted that the current weighted average maturity of the

Federal Reserve’s Treasury holdings was

shorter than at the beginning of the previous normalization episode as of

2014. Some observed that, as a result, depending on the size of any caps put on

the pace of runoff, the balance sheet could potentially shrink faster than last

time if the Committee followed its previous approach in phasing out the

reinvestment of maturing Treasury securities and principal payments on agency

MBS. … they noted that current conditions included a stronger economic outlook,

higher inflation, and a larger balance sheet and thus could warrant a

potentially faster pace of policy rate normalization. They emphasized that the

decision to initiate runoff would be data dependent.

Well, the devil

is always buried in details;

So, for the

average bread consumer need to be explained few things; First of all; the

meaning for Balance Sheet Runoff; -

Banks can experience runoff when individuals and businesses withdraw capital to

invest in other higher-paying investments, thereby reducing the bank's total

capital. But in case of Federal Reserve the story is similar. For example,

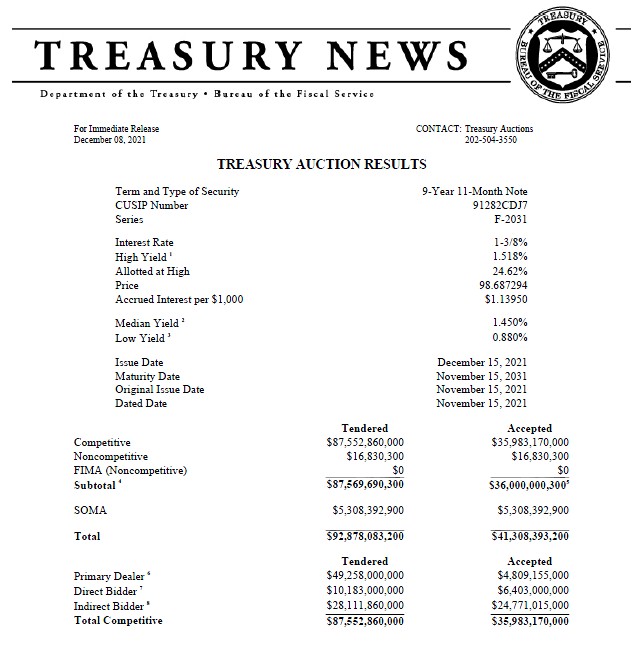

please take a look to latest data of securities at auction (The U.S. Government currently auctions

several Treasury securities to finance the public debt including bills, notes,

bonds, Treasury Inflation Protected Securities (TIPS), and Floating Rate Notes

(FRNs)), where the participants are accepted only for 1/3 of offers or about

35% of those offers as tendered. This further means that the Primary Dealers and

its equivalents as Hedge Funds etc. by requesting certain condition as

participation in bids or not participating at all … in reality as individuals

and businesses withdraw capital to invest in other higher-paying investments.

And that further means the pace of runoff, the balance sheet could potentially

shrink faster than last time as 2014.

Please make a

click on each image for the reality of the Gov. auction in sequence; December 21, 2021 19-Year 11-Month Bond

– Primary Dealers participate in 38,53%; December 08, 2021 9-Year 11-Month Note

- Primary Dealers participate in 41,09%; December 22, 2021 4-Year 10-Month TIPS

- Primary Dealers participate in 41,17%; December 27, 2021 2-Year Note - Primary

Dealers participate in 39,05%; December

29, 2021 119-Day Bill - Primary Dealers participate in 29,34%; December 22, 2021 119-Day Bill -

Primary Dealers participate in 28,58%; December 15, 2021 119-Day Bill -

Primary Dealers participate in 33,14%; December 20, 2021 78-Day Bill - Primary

Dealers participate in 34,78%; December

30, 2021 56-Day Bill - Primary Dealers participate in 31,73%; December 30, 2021 28-Day Bill - Primary

Dealers participate in 37,19%; December

17, 2021 23-Day Bill - Primary Dealers participate in

36,85%.

Many participants

of the Federal Open Market Committee and the Board of Governors of the Federal

Reserve System as of Dec. 2021 judged that the appropriate pace of balance sheet

runoff would likely be faster than it was during the previous normalization

episode (2014). Many participants also judged that monthly caps on the runoff of

securities could help ensure that the pace of runoff would be measured and

predictable, particularly given the shorter weighted average maturity of the

Federal Reserve’s Treasury security holdings. Some participants expressed the

view that the Standing Repo Facility (SRF) would help ensure interest rate

control as the size of the balance sheet approached its longer-run level;

several participants noted that the Standing Repo Facility (SRF) could

facilitate a faster runoff of the balance sheet than might otherwise be the

case; several participants raised the possibility that the establishment of the

Standing Repo Facility (SRF) could reduce the demand for reserves in the longer

run, suggesting that the longer-run balance sheet could be smaller than

otherwise. To achieve such a composition, some participants favored reinvesting

principal from agency MBS into Treasury securities relatively soon or letting

agency MBS run off the balance sheet faster than Treasury securities. The

near-term outlook was revised up, reflecting faster-than-expected increases both

for a broad array of consumer prices and for wages. Supply chain bottlenecks

were seen as continuing to put upward pressure on prices.

Many participants

of the Federal Open Market Committee and the Board of Governors of the Federal

Reserve System as of Dec. 2021 judged that the appropriate pace of balance sheet

runoff would likely be faster than it was during the previous normalization

episode (2014). Many participants also judged that monthly caps on the runoff of

securities could help ensure that the pace of runoff would be measured and

predictable, particularly given the shorter weighted average maturity of the

Federal Reserve’s Treasury security holdings. Some participants expressed the

view that the Standing Repo Facility (SRF) would help ensure interest rate

control as the size of the balance sheet approached its longer-run level;

several participants noted that the Standing Repo Facility (SRF) could

facilitate a faster runoff of the balance sheet than might otherwise be the

case; several participants raised the possibility that the establishment of the

Standing Repo Facility (SRF) could reduce the demand for reserves in the longer

run, suggesting that the longer-run balance sheet could be smaller than

otherwise. To achieve such a composition, some participants favored reinvesting

principal from agency MBS into Treasury securities relatively soon or letting

agency MBS run off the balance sheet faster than Treasury securities. The

near-term outlook was revised up, reflecting faster-than-expected increases both

for a broad array of consumer prices and for wages. Supply chain bottlenecks

were seen as continuing to put upward pressure on prices.

At this point the

average bread consumer shall understand that the Standing Repo Facility (SRF)

could reduce the demand for reserves in the longer run. At its July 2021

meeting, the Federal Open Market Committee (FOMC) established the SRF to serve

as a backstop in money markets to support the effective implementation and

transmission of monetary policy and smooth market functioning. Current effect …

no REPO contracts at all and just Reverse REPO contract are made to manipulate

the value of the dollar on international level and keep inflation as low as

possible on national level. If it raises interest rates, that raises the U.S.

debt-service costs. By stopping buying the securities the FED’s also knows …

that if it tightens monetary policy, i.e. stop asset purchases and raise rates,

debt-burdened will face severe challenges.

At this point the

average bread consumer shall understand that the Standing Repo Facility (SRF)

could reduce the demand for reserves in the longer run. At its July 2021

meeting, the Federal Open Market Committee (FOMC) established the SRF to serve

as a backstop in money markets to support the effective implementation and

transmission of monetary policy and smooth market functioning. Current effect …

no REPO contracts at all and just Reverse REPO contract are made to manipulate

the value of the dollar on international level and keep inflation as low as

possible on national level. If it raises interest rates, that raises the U.S.

debt-service costs. By stopping buying the securities the FED’s also knows …

that if it tightens monetary policy, i.e. stop asset purchases and raise rates,

debt-burdened will face severe challenges.

As an effect of

those factors Janet Yellen the Treasury Secretary simply disappear from view.

She did not tweet nor she

As an effect of

those factors Janet Yellen the Treasury Secretary simply disappear from view.

She did not tweet nor she

By Peter von Roggenhausen Jan. 06 2022.