Is the sleepy Joe … Biden as the very first illegitimate POTUS - Build Back Better – agenda currently set to motion?

The entire problem of the US economy comes with

the FOMOC Committee as the members of this committee have no clue … what they

are doing … and the law makers as member of US Congress has no clue what the

FOMOC Committee is doing as well.

On

Jan. 30, 2019, the Federal Open Market Committee of the Federal Reserve System

announced to little fanfare a momentous change in how it conducts monetary

policy. The change was adopted without

any formal notice or request for public comment, nor with any formal input from

Congress or the Administration.

Nevertheless, the change has had and will continue to have a profound

effect on the role of the Federal Reserve in the United States financial

system. To implement policy in its new

regime, the Fed not only has to be much bigger but also must continuously grow

larger and expand the breadth of its counterparties. The record indicates that the FOMC did not

appreciate the consequences of its decision at the time, and the question now is

whether the decision will be revisited given how manifest and serious those

consequences are. Specifically, the Fed announced that it would conduct monetary

policy by over-supplying liquidity to the financial system, driving short-term

interest rates down to the rate that the Fed pays to sop the liquidity back

up. Previously, the Fed had kept reserve

balances (bank deposits at the Fed) just scarce enough that the overnight

interest rate was determined by transactions between financial institutions;

those transactions consisted of banks with extra liquidity lending to those that

needed it. Now the rate is determined by

transactions between banks and the Fed.

Moreover, the Fed has committed to providing so much extra liquidity that

it would not need to adjust the quantity of reserve balances it is supplying in

response to transitory shocks to liquidity supply and demand. The floor system

is not working well. It has not made

monetary policy implementation easier nor interest rate control better. Instead, it has required the Fed to keep

growing and expanding its set of counterparties.

On

Jan. 30, 2019, the Federal Open Market Committee of the Federal Reserve System

announced to little fanfare a momentous change in how it conducts monetary

policy. The change was adopted without

any formal notice or request for public comment, nor with any formal input from

Congress or the Administration.

Nevertheless, the change has had and will continue to have a profound

effect on the role of the Federal Reserve in the United States financial

system. To implement policy in its new

regime, the Fed not only has to be much bigger but also must continuously grow

larger and expand the breadth of its counterparties. The record indicates that the FOMC did not

appreciate the consequences of its decision at the time, and the question now is

whether the decision will be revisited given how manifest and serious those

consequences are. Specifically, the Fed announced that it would conduct monetary

policy by over-supplying liquidity to the financial system, driving short-term

interest rates down to the rate that the Fed pays to sop the liquidity back

up. Previously, the Fed had kept reserve

balances (bank deposits at the Fed) just scarce enough that the overnight

interest rate was determined by transactions between financial institutions;

those transactions consisted of banks with extra liquidity lending to those that

needed it. Now the rate is determined by

transactions between banks and the Fed.

Moreover, the Fed has committed to providing so much extra liquidity that

it would not need to adjust the quantity of reserve balances it is supplying in

response to transitory shocks to liquidity supply and demand. The floor system

is not working well. It has not made

monetary policy implementation easier nor interest rate control better. Instead, it has required the Fed to keep

growing and expanding its set of counterparties.

On

one level, the story of President Biden's first year is a simple one: Americans

feel worse about the pandemic and economy than they did earlier in his term, and

his ratings have suffered for it. Majorities say he isn't paying enough

attention to either the economy or inflation — together, their top issues — not

just that he isn't handling them well. His overall approval at the one-year mark

is 44%, and it's been in the 40s since this fall. That is, however, despite the

fact that only 26% of Americans think things in the country are going well. Mr.

Biden saw his approval drop months ago without a subsequent recovery. At the

start of his term, his rating was up in the 60s, buoyed by optimism about

getting the pandemic under control. The honeymoon had faded by summer. Dear Joe

Biden money are not leaves and does not grown on trees.

On

one level, the story of President Biden's first year is a simple one: Americans

feel worse about the pandemic and economy than they did earlier in his term, and

his ratings have suffered for it. Majorities say he isn't paying enough

attention to either the economy or inflation — together, their top issues — not

just that he isn't handling them well. His overall approval at the one-year mark

is 44%, and it's been in the 40s since this fall. That is, however, despite the

fact that only 26% of Americans think things in the country are going well. Mr.

Biden saw his approval drop months ago without a subsequent recovery. At the

start of his term, his rating was up in the 60s, buoyed by optimism about

getting the pandemic under control. The honeymoon had faded by summer. Dear Joe

Biden money are not leaves and does not grown on trees.

As an outcome we are - Fellow

members of the US Bankruptcy. The US Treasury, Federal Reserve and current

administration of the White House try everything possible to make honest dollar;

Markets Raffles, Markets bazaars and block parties as for that instance oncoming

Feb. 26 2022 George Washington birthday ball. Now, we all know that business has

been rotten lately. So, to furnish US with the details I will call the body in

charge of the rotten business FOMOC Committee which shall read the statement for

our current fiscal year reads as follows; - “we’re busted”

But instead the FOMOC Committee issues two

different minutes from November and December 2021.

In the first article (click on the

image to the right) we

have explained as “Balance Sheet Runoff” where we have pointed

that Primary Dealers being tied of forced investment in Treasury securities, have move these

liquidities to other business operation and currently the Treasury run on

deficit about 100 trillion dollars as virtual fund desperately needed for the

futures maturity dates of the mentioned treasury securities. Considering

additional fact that the intention is to stop asset purchase will cause the

disaster with raising cost as debt service we are at the very edge of the

financial cliff. Today I will have corroborated not just the future financial

situation of the US Treasury but the date described by FOMOC Committee as “resulting in an end to net asset purchases

in mid-March” which in reality shall be interpreted as financial collapse

date.

In the first article (click on the

image to the right) we

have explained as “Balance Sheet Runoff” where we have pointed

that Primary Dealers being tied of forced investment in Treasury securities, have move these

liquidities to other business operation and currently the Treasury run on

deficit about 100 trillion dollars as virtual fund desperately needed for the

futures maturity dates of the mentioned treasury securities. Considering

additional fact that the intention is to stop asset purchase will cause the

disaster with raising cost as debt service we are at the very edge of the

financial cliff. Today I will have corroborated not just the future financial

situation of the US Treasury but the date described by FOMOC Committee as “resulting in an end to net asset purchases

in mid-March” which in reality shall be interpreted as financial collapse

date.

A joint meeting

of the Federal Open Market Committee and the Board of Governors of the Federal

Reserve System was held by videoconference on Tuesday, December 14, 2021, at

9:00 a.m. and continued on Wednesday, December 15, 2021, at 9:00 a.m. The

meeting adjourned at 11:00 a.m. on December 15, 2021. But the minutes of this

meeting were released on January the 5 2022. It was agreed that the

next meeting of the Committee would be held on Tuesday–Wednesday, January 25–26,

2022. In response, the Propaganda Machine as Reuters for that instance followed

by Bloomberg, CNBC or Fox News etcetera, imprinted to general bread consumers

reality perception that the strengthening economy and higher inflation could

lead to earlier and faster interest-rate increases than previously expected,

with some policy makers also favoring starting to shrink the balance sheet soon

after.

But what they as

the Propaganda Machine shall tell for you … goes like

this;

Beginning in

January, the Committee will increase its holdings of Treasury securities by at

least $40 billion per month and of agency mortgage-backed securities by at least

$20 billion per month. Increase the SOMA holdings of Treasury securities as

described, during the monthly purchase period beginning in mid-January.

Regarding the outlook for U.S. monetary policy, expectations for a reduction in

policy accommodation shifted forward notably. Respondents to the Open Market

Desk’s surveys of primary dealers and market participants broadly projected that

the Committee would quicken the pace of reduction in the Federal Reserve’s net

purchases of Treasury securities and agency mortgage-backed securities (MBS),

and the median respondent projected net asset purchases to end in March 2022.

The median respondent’s projected timing for the first increase in the target

range for the federal funds rate also moved earlier from the first quarter of

2023 to June 2022 according to the November minutes. But to understand that we have to focus on

November policy prediction and subsequent performance;

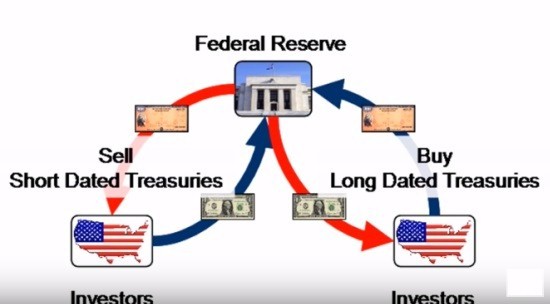

In November reductions

intention in the Federal Reserve’s net purchases of Treasury securities and

agency mortgage-backed securities (MBS) pace which subsequently were

implemented, the System Open Market Account (SOMA) portfolio (click

on the image to the left for details) shall peak around next

June at about $8.5 trillion. In reality this happened in January 2022. And what

was not anticipated at November FOMOC Committee

was the default as burden of this intention. The Treasury used the Rollovers

tool to balance the finance of the GOV. A SOMA Treasury rollover describes the

process by which principal payments from maturing Treasury securities held by

the SOMA are reinvested in newly auctioned securities. Specifically, the Open

Market Trading Desk at the Federal Reserve Bank of New York places

non-competitive bids at Treasury auctions, in an amount equal to all or a

portion of the maturing Treasury securities, that will settle on the maturity

date of the maturing Treasury securities. On the auction settlement date, the

maturing Treasury securities are exchanged for the newly issued Treasury

securities. But this operation at the very same time does create deficit in

liquidity portfolio redirecting all operation to bankruptcy definition. In other

words, the overnight loan, be granted upon participation in this process. Quote

from Federal Reserve Bank of NY; “Loans are awarded based on competitive bidding

in a multiple price auction for each security. Primary dealers that have elected

to participate in the program may submit bids via FedTrade after the auction has been announced. Loan awards

are constrained by dealer limits. In addition, the New York Fed reserves the right to reject

bids at its discretion, when it is believed that granting the loan would

facilitate a dealer’s ability to control

a specific issue.”

In November reductions

intention in the Federal Reserve’s net purchases of Treasury securities and

agency mortgage-backed securities (MBS) pace which subsequently were

implemented, the System Open Market Account (SOMA) portfolio (click

on the image to the left for details) shall peak around next

June at about $8.5 trillion. In reality this happened in January 2022. And what

was not anticipated at November FOMOC Committee

was the default as burden of this intention. The Treasury used the Rollovers

tool to balance the finance of the GOV. A SOMA Treasury rollover describes the

process by which principal payments from maturing Treasury securities held by

the SOMA are reinvested in newly auctioned securities. Specifically, the Open

Market Trading Desk at the Federal Reserve Bank of New York places

non-competitive bids at Treasury auctions, in an amount equal to all or a

portion of the maturing Treasury securities, that will settle on the maturity

date of the maturing Treasury securities. On the auction settlement date, the

maturing Treasury securities are exchanged for the newly issued Treasury

securities. But this operation at the very same time does create deficit in

liquidity portfolio redirecting all operation to bankruptcy definition. In other

words, the overnight loan, be granted upon participation in this process. Quote

from Federal Reserve Bank of NY; “Loans are awarded based on competitive bidding

in a multiple price auction for each security. Primary dealers that have elected

to participate in the program may submit bids via FedTrade after the auction has been announced. Loan awards

are constrained by dealer limits. In addition, the New York Fed reserves the right to reject

bids at its discretion, when it is believed that granting the loan would

facilitate a dealer’s ability to control

a specific issue.”

In terms of

composition, Treasury securities and agency MBS would constitute roughly 70

percent and 30 percent of the SOMA portfolio, respectively—roughly in line with

the shares of Treasury securities and agency MBS in the total stock of these

securities outstanding—and the SOMA portfolio would be more heavily weighted

toward Treasury securities than after the conclusion of the third large-scale

asset purchase program 2014 following the global financial crisis. Participants

also expected that economic conditions would evolve in a manner such that

similar reductions in the pace of net asset purchases would be appropriate each

subsequent month, resulting in an end to net asset purchases in mid-March, a few

months sooner than participants had anticipated at the November FOMC meeting.

Members also agreed that similar reductions in the pace of net asset purchases

would likely be appropriate in subsequent months, implying that increases in the

Federal Reserve’s securities holdings would cease by mid-March under the

Committee’s outlook, a few months sooner than had been anticipated at the

previous meeting.

In terms of

composition, Treasury securities and agency MBS would constitute roughly 70

percent and 30 percent of the SOMA portfolio, respectively—roughly in line with

the shares of Treasury securities and agency MBS in the total stock of these

securities outstanding—and the SOMA portfolio would be more heavily weighted

toward Treasury securities than after the conclusion of the third large-scale

asset purchase program 2014 following the global financial crisis. Participants

also expected that economic conditions would evolve in a manner such that

similar reductions in the pace of net asset purchases would be appropriate each

subsequent month, resulting in an end to net asset purchases in mid-March, a few

months sooner than participants had anticipated at the November FOMC meeting.

Members also agreed that similar reductions in the pace of net asset purchases

would likely be appropriate in subsequent months, implying that increases in the

Federal Reserve’s securities holdings would cease by mid-March under the

Committee’s outlook, a few months sooner than had been anticipated at the

previous meeting.

The entire problem is less

complicated than that. The Government may have plenty of money for every issue

as they may come-up with and do to the fact as US economy comes with the FOMOC

Committee as the members of this committee have no clue … what they are doing …

and the law makes as member of US Congress has no clue what the FOMOC Committee

is doing as well. If there be just few Members of the Congress with open mind we

can solve the debt – deficit and monetary policies within a week or so. But we

have to get rid of the sleepy Joe first and let open mind personnel to govern

the country.

By Peter von Roggenhausen Jan. 20 2022.