How bad is the world financial situation?

Nations

who maintain their own currency and whose debt is denominated in that currency

will have the option to implicitly default by inflating their currency via

printing more money to cover the outstanding portion. Of course, not all

defaults are the same. In some cases, the government misses an interest or

principal payment. Other times, it merely delays a disbursement. The government

can also exchange the original notes for new ones with less favorable terms.

Though not common, countries can, and periodically do, default on their

sovereign debt. This happens when the government is either unable or unwilling

to make good on its fiscal promises to repay its bondholders. Greece, Argentina, Russia,

and Lebanon are just a few of the governments that have defaulted over the past

decades.

Historically,

failure to make good on loans is a bigger problem for countries that borrow in a

foreign currency instead of using their own. An event of default is a predefined

circumstance that allows a lender to demand full repayment of an outstanding

balance before it is due. In many agreements, the lender will include a contract

provision covering events of default to protect itself in case it appears that

the borrower will not be able to or does not intend to continue repaying the

loan in the future. An event of default enables the lender to seize any

collateral that has been pledged and sell it to recoup the loan. This often is

employed if the default risk is beyond a certain point.

Sovereign

default is a failure by a government in repayment of its country's debts.

Countries are typically hesitant to default on their national debts, since doing

so will make borrowing funds in the future difficult and more expensive.

However, sovereign countries are not subject to normal bankruptcy laws and have

the potential to escape responsibility for debts, often without legal

consequences.

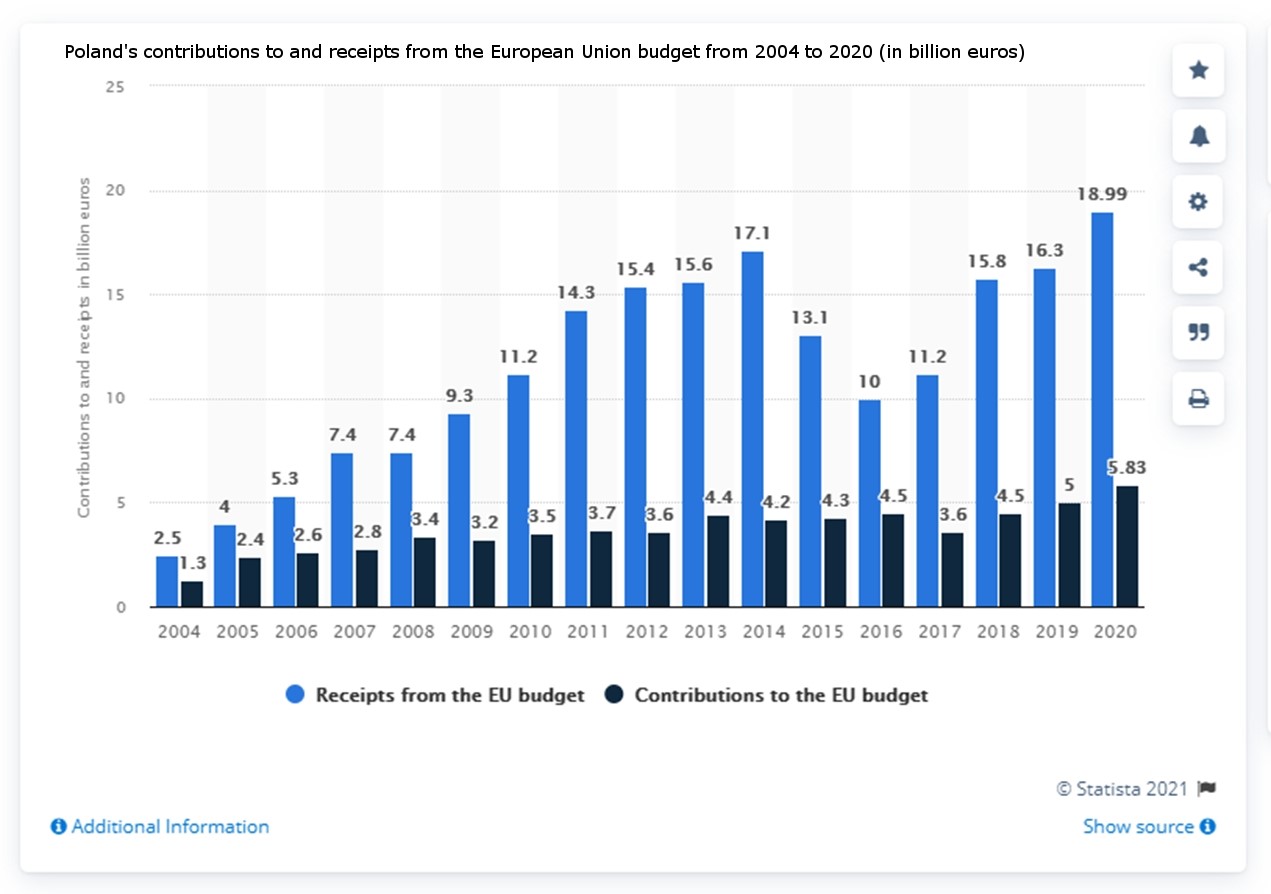

For that instance, I will show for you how bad it is in European Union;

An issue in this case be measured in Billions of Euro’s. So, Like Biden EU fall short in liquidity and to cover its default as missing payment and at the same time to avoid market panic.

For

that instance, EU decide to reduce as delay payment of 57 billion Euro for/to

Poland and blame the Poland's challenge to the primacy of European Union law

over national law but in case of Hungary with similar sum of money the EU not

just blame the Hungarian Nation, but also European Union officials suggesting

further delays are in store for post-pandemic aid.

The trick goes with new income to EU from the member states as what was delay 2020 budget then the 2021 budget be compensated and in liquidity market well covered.

The eastern European nations are among a dwindling group of member states that have yet to receive approval for their plans to spend their shares of the bloc’s virus stimulus package. European Commission Vice President Valdis Dombrovskis said last week the EU executive is seeking additional clarification from them about their compliance with the conditions of the aid. Euro zone inflation could exceed expectations in the short and medium term, and this outlook for price growth warrants an end to the European Central Bank's emergency bond purchases next March, Dutch central bank chief Klaas Knot said on Thursday.

In

the US the debt ceiling increase of about $500 billion through Dec. 3 passed the

Senate last week and the House on Tuesday. US come-up also with the Standing

Repo Facility (SRF) which serves as a backstop to dampen upward interest rate

pressures that can occasionally emerge in overnight U.S. dollar funding markets

and spillover into the fed funds market. The Desk generally conducts both the ON

RRP and SRF operations each business day.

While Overnight Reverse Repo Facility reduce the cash overnight to avoid high inflation is only a cosmetic trick to run the financial system. The Federal Reserve manages overnight interest rates by setting the interest on reserve balances (IORB) rate, which is the rate paid to depository institutions on balances maintained at Federal Reserve Banks. The ON RRP provides a floor under overnight interest rates by offering a broad range of financial institutions that are ineligible to earn IORB, an alternative risk-free investment option. Additionally, the Fed is considering the creation of a standing repo facility, a permanent offer to lend a certain amount of cash to repo borrowers every day. It would put an effective ceiling on the short-term interest rates; no bank would borrow at a higher rate than the one

Richmond Federal Reserve President Tom Barkin on Thursday said the U.S. central bank has cleared a path for what he hopes to be a "seamless" start to a reduction in its support for the economy, but that it will take more time to determine when interest rate hikes will be appropriate.

JPMorgan

Chase & Co (NYSE:JPM), Citigroup (NYSE:C), Well

Fargo & Co and Bank of America Corp (NYSE:BAC), seen by analysts and

economists as bellwethers of the broader economy, reported a combined profit of

$28.7 billion for the third quarter,

The

U.S. and UK bond markets are sounding the economic alarm

bell.

Yield

curves in both markets are flattening dramatically, indicating that traders are

pricing in a growing risk of a central bank policy error or an increasingly

gloomy outlook for long-term growth.

Yield

curves flatten when the gap between short- and longer-dated borrowing costs

shrinks, and they invert when longer-term yields fall below shorter-dated

yields. Both scenarios, particularly inversion, often precede slowing growth and

sometimes recession.

Group

of Seven advanced economies said on Wednesday this week that any digital

currency issued by a central bank must "support and do no harm" to the bank's

ability to fulfill its mandate on monetary and financial stability, and must

also meet rigorous standards. This financial tool is no longer needed as before

2014 since there’s no solution on supply side of the financial situation to

remove overflooded cash from the system.